Earnings Beat Sends Shares Soaring

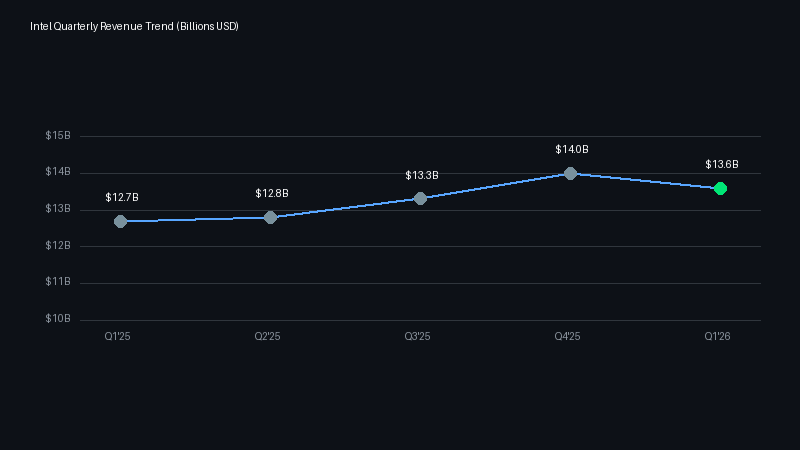

Intel reported first-quarter 2026 revenue of $13.6 billion, handily beating the $12.4 to $12.8 billion range Wall Street analysts had projected. The surprise sent the stock up 50% in after-hours trading — one of the biggest single-day jumps in recent memory. Investors are finally seeing green shoots from CEO Pat Gelsinger’s multiyear turnaround plan.

The earnings beat came from strength across multiple segments, with the Data Center and AI division posting 22% year-over-year growth leading the way. Even the most optimistic forecasters hadn’t penciled in a number this high.

Data Center and AI Drives Growth

The DCAI segment was the standout performer, growing revenue 22% year over year. Enterprise demand for AI inference chips and a rebound in hyperscaler cloud spending — which had sagged through 2025 — fueled the jump.

Intel’s next-gen Xeon processors, built on the company’s advanced process nodes, are finally pulling share away from AMD and ARM-based rivals. The division is now the largest single segment in Intel’s portfolio, which tells you everything about where the company’s bets are placed.

The Client Computing Group turned in strong numbers too, riding the AI PC refresh cycle. AI-capable PCs are selling faster than previous upgrade cycles, and as the dominant x86 supplier, Intel has caught most of that wave.

Foundry Losses Narrow, But Profitability Remains Distant

The real spotlight landed on Intel Foundry Services (IFS). The segment — Intel’s attempt to become a contract chipmaker for external clients — posted operating losses 16% narrower than the previous quarter. Still bleeding money, sure, but it’s the first consistent quarter-over-quarter improvement the division has ever posted.

Gelsinger called it “early validation of our IDM 2.0 strategy” on the earnings call, pointing to rising external customer engagement and several major design wins heading toward volume production. He was careful to note, though, that profitability is still a ways off.

The foundry bet is all or nothing for Intel. Gelsinger’s plan to compete with TSMC and Samsung in contract manufacturing requires billions more in capital spending. The narrowing losses are a good sign — the strategy isn’t broken — but nobody knows when the division will actually turn profitable.

What Could Go Wrong

The market’s enthusiasm is understandable, but Intel still has hurdles. The foundry will keep burning cash for several more quarters, and TSMC’s lead in advanced-node manufacturing is not something you erase overnight. Samsung isn’t sitting still either.

Then there’s the valuation question. A 50% pop in a single session bakes a lot of optimism into the stock price. Intel’s now trading as if the foundry turnaround is already done — and it isn’t.

Still, Q1 2026 was Intel’s best quarter in a while. The AI tailwinds are real, the data center business is growing, and the foundry is bleeding less. Whether the stock deserves this re-rating comes down to one thing: can Intel keep this up?

References

- Intel Q1 2026 Earnings Release: https://www.intc.com/investor-relations/earnings

- Intel Foundry Services Overview: https://www.intel.com/foundry

- Semiconductor Industry Association Data: https://www.semiconductors.org

- Reuters: “Intel shares surge after earnings beat expectations” https://www.reuters.com/technology/intel-earnings

- Bloomberg: “Intel’s Foundry Strategy Shows First Signs of Life” https://www.bloomberg.com/news/intel-foundry